Blog

2025 Year Ahead Outlook: Built to Last

We hedge our bets, here at Infinium. A ‘Year Ahead Outlook’ piece published in early February is pushing it a little, don’t you think? We cannot disagree. But, maybe this year, it’s warranted.

Politics Purgatory

The number one reason we delayed this note is due squarely to the political environment and the transition of power that occurred three short weeks ago. Like him or not, it’s safe to say there hasn’t been a more polarizing figure in American politics than the current President, at least in modern times.

We have received an extraordinary amount of inquiries in this past week, especially, given the tariffs that Trump threatened against Mexico, Canada, and China (see our recent blog post, Trump’s Tariffs Explained.) To say this has caused uneasiness with a segment of our clients might be the understatement of year. Plain and simple, we wanted to see the new administration take charge before peering into the crystal ball.

Nothing to see here

Curiously enough, here in the first week of February, the U.S. stock markets are positive by approximately 2.5%, and gold is the big winner at +9% (we recently doubled our gold exposure in portfolios in many accounts). Bonds continue to struggle with an average return under 1% so far year-to-date. The Alternatives we use, (generally Managed Futures funds), are right there with stocks at +4% or so. Overall, this is hardly a market that is asking us to reduce risk, yet by the reaction of many investors, one would think the markets are taking a hit.

Emotion vs Reality

We all know that how we perceive a situation is our reality. Two people can view the same movie and have vastly differing opinions about the plot, characters, and the quality of the film. The same holds true for the markets and how an investor might view the current investing landscape in light of uneasiness with American politics today. There’s an entire swath of investors who look at what’s going on and love it, by the way. None of those investors are contacting us asking for less risk, and they have been correct. Doesn’t mean they will ultimately be correct, however.

One of the most important values we can add to any client, particularly those that are concerned today about how politics might negatively affect their portfolios, is to provide insight into what IS vs what ISN’T. By reacting to the changes in the markets that should be acted upon, and not on situations that could happen, we are in a position of strength for you. Our goal is to set aside our biases, whatever those may be, and make sound judgements on your behalf. It’s a challenge we readily accept.

To Sell or Not to Sell

I want to be clear here, there are times where swift and decisive action is needed to prevent losses. Today, that is not the case with the markets. There is nothing especially interesting or noteworthy about the returns so far in 2025.

If I told you on January 1 that the stock markets would be up by 2-3% and everything else in positive territory in five weeks, would you be concerned and want to reduce risk?

I sure hope not. We would highly encourage you to not do so, if that was the request. There is nothing in prices that tell us to take less risk, in fact, it’s quite the opposite. When we see the investing public rather worried and holding back, that typically corresponds to a great time to be adding risk to a portfolio. This is one of the great conundrums of investing. It’s hard to explain that, when we feel the most uneasy as a group, this is usually a low-risk time to try and grow a portfolio. I have seen this over the past 26 years as a financial advisor, and it always astounds me as much today as it did back in the Tech Bubble of the late 1990s when I started.

Survey says…

Make no mistake, it’s hard to imagine calm when Trump is at the wheel, let’s be honest here. We fully expect 2025 to be a wild ride, yet not necessarily one that causes damage to portfolios. As I have shared with many of you, we are in an enviable position to be able to shift portfolios around quickly if needed. Additionally, we have the tools to make money no matter if the markets are up or down.

I repeat, we have the ability and investment strategies available to us which allow for navigating successfully through any and all market conditions. This is one of the great differentiators between Infinium and most other investment companies.

We are committed to keeping your portfolios in the right place, no matter where that right place is at any given time. Does this mean we will not see negative returns? Of course not. But we will take action and go to places like Managed Futures (see our recent blog post Managed Futures for Dummies) and gold if those areas are working and everything else is not. In essence, we look to construct portfolios that are built to last, but not static by any measure. Sadly, the industry at large likes to do that; to put the burden on you to accept the results of a static mix matter what is going on. We choose the road less traveled. The one where a dynamic allocation to various parts of the market result in a smoother, and more sensible way to navigate through the volatility.

So what does the rest of 2025 look like from our perch:

Stock Market

- Can we get another double-digit return after +20% each of the past two years? This seems like a stretch, yet for now, we are fully allocated to our models given the positive momentum over the past five weeks.

- The potential for volatility due to the aforementioned geopolitical risks and interest rate fluctuations. As long as the trend in stocks remains up or neutral, we are likely to remain fully allocated to our weightings in this area. Recall, despite the scary headlines and volatility during Trade War 1.0 (2018-2019), the S&P 500 still appreciated 20% over these two years.

- This is the most volatile part of any portfolio, usually, so you are likely to see more changes and shifts here than in other buckets within your portfolio.

Bond Market

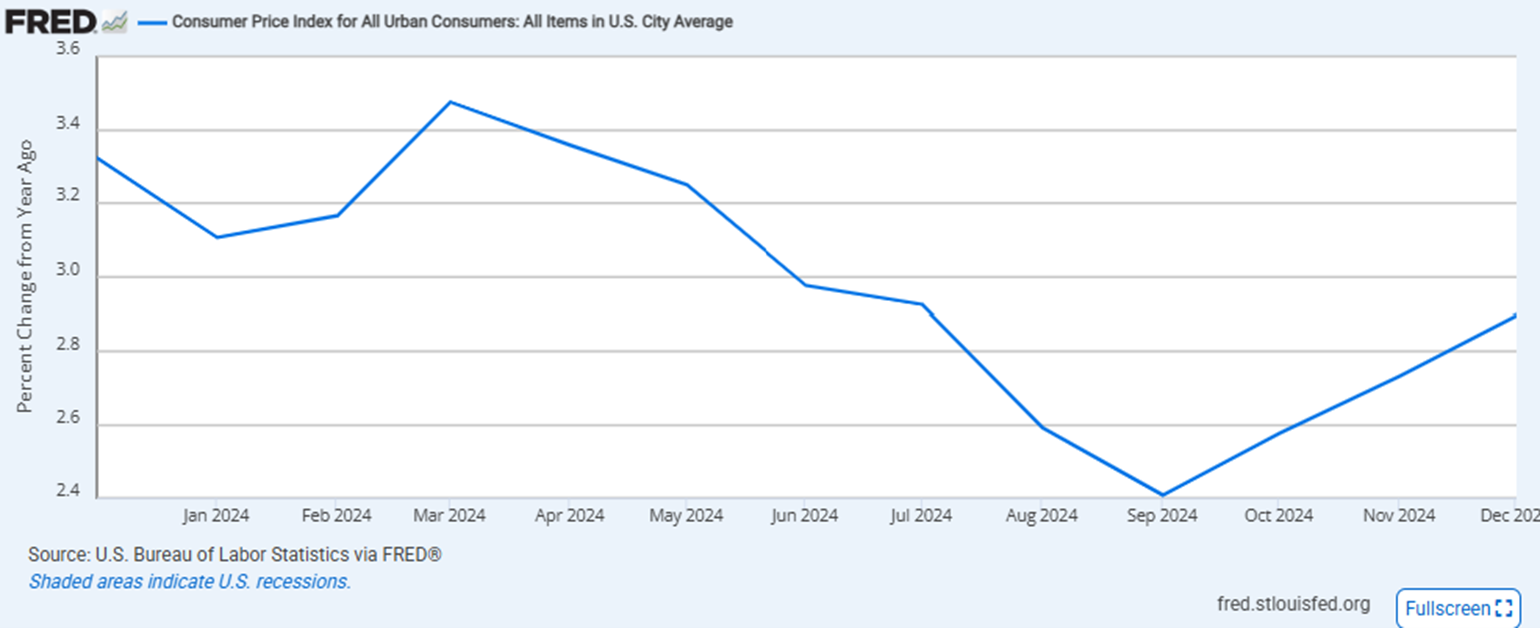

- Persistent, and now re-accelerating inflation each month since September of last year (see chart below of year-over-year percentage change of CPI published by the St. Louis Fed), should continue to put upward pressure on interest rates and thus beget lower bond prices. The spectre of tariffs are also likely inflationary and adds another tailwind toward higher interest rates.

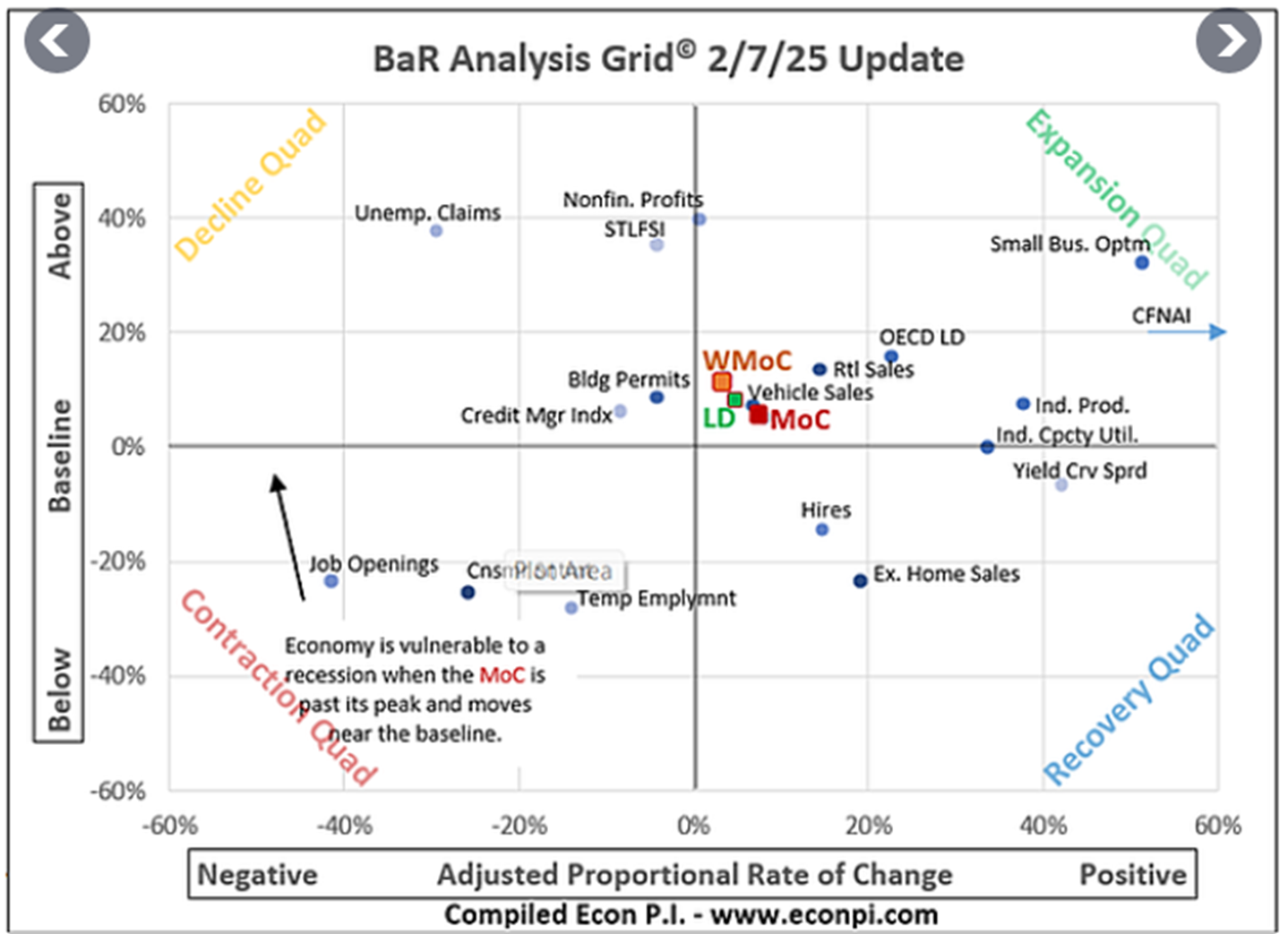

- Along with sticky inflation & tariffs, our preferred measure to analyze the state of the economy (see chart below from Econpi.com), has continued to show an economy in expansion since the fall of last year. Sticky inflation plus an expanding economy is not a recipe for the Fed to cut interest rates anytime soon, yet another boon to interest rates (and negative for bonds).

- As a result of our negative view on bonds, our clients will not see much of those in their portfolios in 2025. On a side note, we were nearly out of bonds last year when those returned a measly 1.3%. The old formula of 60% stocks and 40% bonds has really hurt investors who subscribe to it, and fortunately, no corporate mandates force us into it.

Gold

- Several factors such as inflation, the national debt, economic uncertainty, and geopolitical tensions are all driving gold prices to new all-time highs.

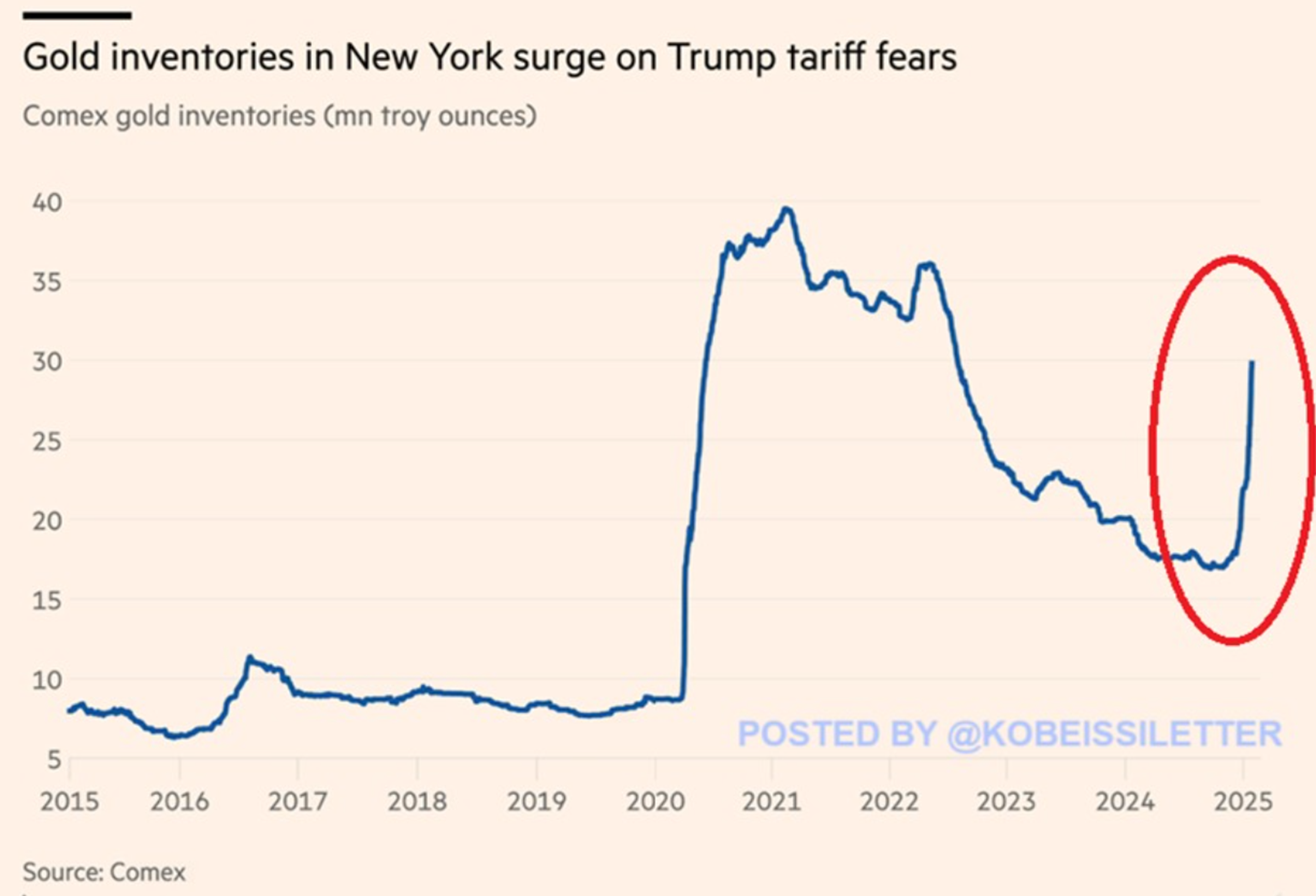

- Most recently, tariff talk has supercharged the year-to-date rally as large buyers on the COMEX, the world’s largest exchange for trading metals operating out of New York, have been taking the most physical delivery of the precious metal since August 2022 and at the fastest rate since the Covid-19 scare and subsequent gold rally in 2020 (see chart below shared by The Kobeissi Letter). This could be buying ahead of possible tariffs, or it could be due to a multitude of other reasons mentioned above, or even that buyers would now rather own physical gold in lieu of gold tracking ETFs for additional safety and security.

- Regardless of the exact reason causing a move in gold at any given time, as long as the national debt continues to increase, as we wrote about extensively in October here (Market Update October 2024: Got Gold), we remain long-term holders of our gold position.

Residential Real Estate

- Residential RE is a victim of heavy government intervention, and now we are seeing the results: record low sales volumes and mortgage demand. Who wants to give up their 2-3% 30-year mortgage for one that’s 300% higher? Not many, clearly.

- Prices are drifting lower, and in the hotter markets, the pace of decline is off -20% or more in places like here in Denver; the bottom is not in just yet.

- We see a slow thawing of the markets even if interest rates remain stubbornly high, simply because life events like job changes, retirement, and death naturally create transaction.

- Current home owners that do stay put will drive demand for remodeling.