Blog

How Wars Shake the Stock Market

Wars have shaped human history for millennia, and they’ve left their mark on financial markets just as dramatically. From the outbreak of World War II to the 2022 Russian invasion of Ukraine and more recent Middle East conflicts, geopolitical shocks consistently trigger volatility in stocks. Yet history shows a surprising pattern: while markets often dip sharply at first, they tend to recover quickly—and frequently deliver solid long-term gains. Understanding these dynamics can help investors navigate uncertainty without panic-selling.

The immediate reaction is almost always fear-driven. When conflict erupts, investors flock to safe-haven assets like gold, U.S. Treasuries, or cash, triggering broad sell-offs. Data from 20 major post-World War II military events analyzed by RBC Wealth Management shows the S&P 500 typically falls about 6% from the initial shock to its trough, with the average bottom reached in roughly 13 trading days. Recovery to pre-event levels usually takes just 28 days. Similar studies from LPL Financial and other firms confirm this: even in serious conflicts, drawdowns average 7% and resolve in under two months. The 1990 Gulf War stands out as an exception—an oil shock drove a deeper 16% decline—but most episodes fade fast once the scope of the fighting becomes clear.

Why the initial plunge? Uncertainty is the enemy of valuation. Investors hate unknowns about duration, escalation risk, and economic spillover. Supply chains can fracture, commodity prices spike, and consumer confidence wanes. Oil is especially sensitive: wars in the Middle East or involving major producers often send crude prices soaring, as seen in 2022 when Russia’s invasion of Ukraine helped push energy costs higher and amplified inflation pressures already building from the pandemic.

Not all sectors suffer equally. Defense and aerospace companies are classic winners. Firms like Lockheed Martin, Northrop Grumman, and Raytheon typically see order backlogs swell as governments ramp up military spending. Energy stocks—particularly oil producers and services—often rally on supply disruptions or heightened geopolitical risk premiums. During the early days of recent Iran-related tensions in 2025, defense and select energy names posted strong gains while the broader market wavered.

On the flip side, consumer discretionary, travel, airlines, and retail stocks usually take a hit. Heightened fear reduces spending on big-ticket items and leisure. Banks and financials can face pressure from rising volatility and potential credit risks if the conflict drags on. Tech sometimes holds up better if it’s viewed as “essential” infrastructure, but broader market risk-off sentiment can drag everything down initially.

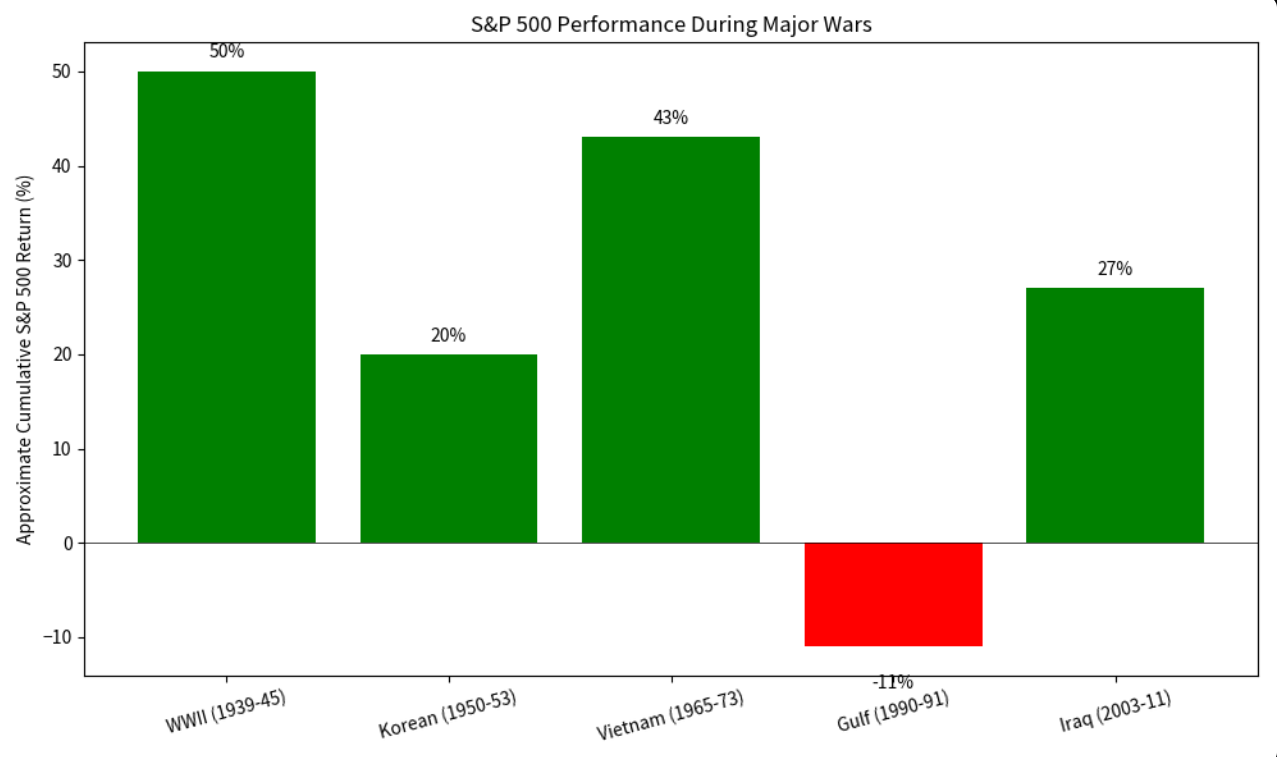

Longer term, the picture brightens considerably. Wars rarely derail the stock market’s upward trajectory for long. During World War II (1939–1945), the Dow Jones Industrial Average rose about 50% overall, or more than 7% annualized, despite the conflict’s scale. The Korean War (1950–1953) delivered annualized returns near 16%. Even the Vietnam era saw the Dow climb roughly 43% from U.S. troop escalation in 1965 through withdrawal in 1973. Post-9/11 and the 2003 Iraq invasion, markets recovered swiftly once uncertainty lifted. Across multiple studies, one-year returns after major conflicts average positive, often in the double digits when the economy remains fundamentally sound.

Several factors explain this resilience. First, governments pour money into defense and infrastructure, creating economic tailwinds. Second, central banks and fiscal authorities often respond with supportive policy—rate cuts, stimulus, or spending—that cushions the blow. Third, markets price in the “known unknowns” quickly; once the fog of war clears, earnings growth and corporate adaptability take over. Small-cap stocks, in particular, have historically outperformed during wartime periods as domestic-focused companies benefit from government contracts and reshoring trends.

Of course, context matters. Wars that coincide with oil shocks, recessions, or monetary tightening (like 2022’s overlap with Fed rate hikes) can prolong pain. Conflicts directly involving the U.S. or its major trading partners tend to matter more than distant skirmishes. And prolonged, multi-year wars introduce inflation and debt risks that can weigh on multiples.

For investors, the lessons are clear. First, avoid knee-jerk reactions—history rewards those who stay invested. Second, consider rebalancing toward sectors that historically thrive: defense, energy, and commodities. Third, maintain diversification across asset classes, geographies, and styles. Gold or inflation-protected securities can act as buffers. Finally, focus on quality companies with strong balance sheets that can weather volatility.

Wars are tragic and unpredictable, but they don’t break the stock market’s long-term upward bias. Markets climb walls of worry because economies adapt, innovation continues, and human ingenuity finds a way forward. The next conflict will bring headlines and heartburn, but disciplined, long-term investors have repeatedly come out ahead. In the end, time in the market still beats timing the market—even when cannons roar.